Malta’s credit landscape is changing. The Credit Review Office Act marks a meaningful shift in how credit relationships between lending institutions and their customers are expected to operate in Malta. Rather than imposing rigid obligations or punitive sanctions, the Act operates as a form of soft law — one designed to foster greater transparency, encourage more structured dialogue, and promote fairer credit practices across the sector. Its introduction signals a broader cultural expectation: that lending decisions should be reasoned, communicated clearly, and open to legitimate scrutiny. Over time, this framework is likely to raise the bar for how institutions document and explain their credit decisions, with a corresponding increase in borrower confidence and, ultimately, a more robust and accountable credit market in Malta.

The Act creates a structured complaint and review process through which eligible applicants — namely, Maltese based sole traders and commercial partnerships — may seek an independent review of certain credit decisions.

The Act’s reach is not unlimited. It excludes from its scope decisions relating to credit facilities in excess of €2,000,000 and those of less than €5,000, and notably, excludes non-performing facilities.

Eligibility under the Act arises where an eligible applicant has either been refused a credit facility; has not received a timely final decision on a request for a credit facility; has had an existing facility formally withdrawn or reduced; has received a formal refusal on a request for the restructuring of an existing credit facility; or has not received a timely final decision on a request for the restructuring of an existing credit facility.

The Charter

The charter is a central function of the Act. Every lending institution is required to draw up a charter setting out, inter alia:

(a) guidance on the credit application process and applicable timelines;

(b) an indicative list of initial documentation and data expected from applicants;

(c) security and collateral requirements, to the extent applicable;

(d) information on the lending institution’s internal complaint handling mechanisms; and

(e) information on the applicant’s right, in certain circumstances, to refer the matter to the CRO for review.

Beyond these core elements, the charter must also set out the timeframe within which the lending institution will inform a customer or potential customer of its decision following a credit application or a restructuring request, and compliance with these requirements is vested with the MFSA.

Notably, where a lending institution fails to draw up and publish its own charter, the default charter set out in the Schedule to the Act applies automatically. Lending institutions are therefore encouraged to prepare a bespoke charter tailored to their own operations — not out of obligation, but rather to set the standard for how credit decisions are communicated and to set a baseline against which the CRO is able to review applications submitted by eligible applicants.

The Review Process

Before approaching the CRO, an eligible applicant must first exhaust the lending institution’s internal process (where available). Recourse to the CRO must be sought within 90 days of the conclusion of that internal process. Once a matter reaches the CRO, the default approach is mediation, though participation is voluntary and either party may withdraw at any time. Proceedings are conducted in private. Where mediation is unsuccessful or declined, the credit reviewer issues a non-binding recommendation and no monetary compensation may be awarded.

The recommendation is strictly confidential and disclosed to the parties only. It may not be shared with or communicated to any third party except as required by law, and both parties are bound by this obligation. Where a lending institution chooses not to comply with the recommendation, it must provide the credit reviewer with its reasons for non-compliance — to the extent permitted by law — and the credit reviewer may elect to share those reasons with the applicant. Statistical data may however be issued by the CRO in its annual report.

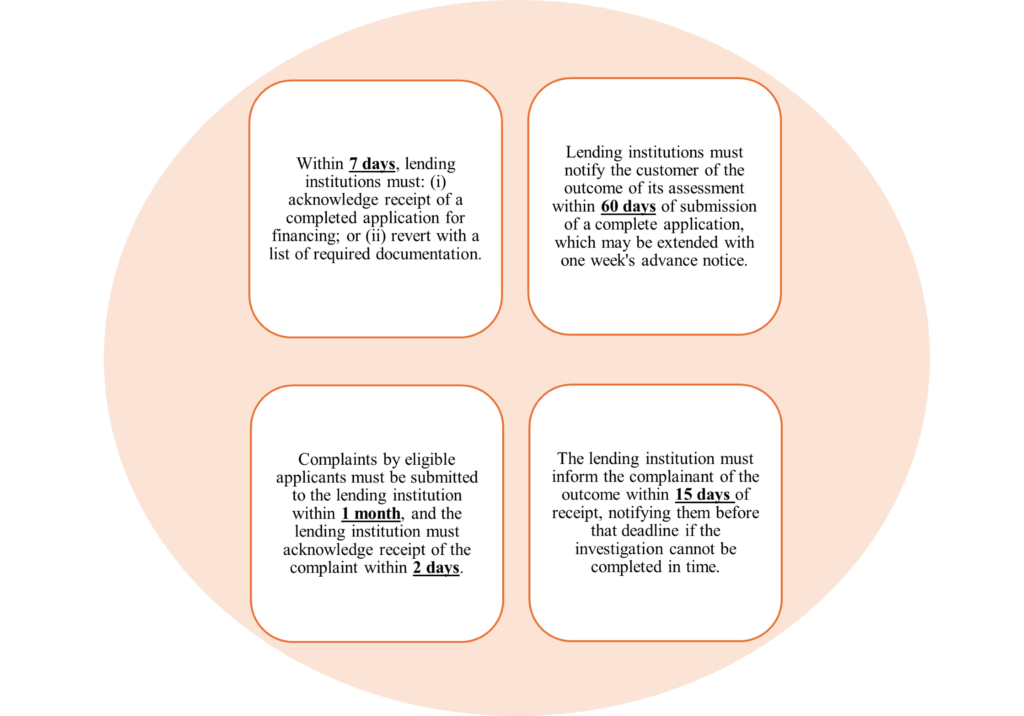

Key Timelines

The following timelines apply under the default charter in the Schedule to the Act:

The charter is not a compliance formality — it is the foundation on which a lending institution’s entire credit review framework rests. A well-drafted, bespoke charter sits at the heart of this new framework. Lending institutions with any questions in relation to their obligations under the Act — and in particular in relation to the institution’s specific operations and risk profile — are welcome to reach out to our team.